casualty US consumer spending and sentiment remains strong, so far.

casualty US consumer spending and sentiment remains strong, so far.

{kind=link}

only a small number of sector leaders turn a profit, insurance was among the industries hardest hit, McKinsey_Website_Accessibility@mckinsey.com, talent acquisition, development, and retention, have significant leverage through interactive tools and data-driven insights, allowing them to handle substantially larger books of business with more precision and control, monitor a mix of leading and lagging indicators to provide portfolio transparency and enable proactive interventionfor example, by using quality as a leading, not lagging, KPI, use data throughout the underwriting process to inform underwriter decisions in prioritization of prospects, validation of exposures, policy structuring, and pricing, rely on continuously evolving risk models that incorporate ever-expanding views of risk characteristics, tailored by line, segment, and emerging-loss trends.  Get the free report to find out everything you need to know about key fintech players, trends, and advancements. Before predictive analytics, insurers could estimate or take guesses at these questions, but now they are able to accurately and effectively service customers, which ultimately results in happier customers and increased revenues. Achieving underwriting excellence ultimately hinges on having highly trained and motivated staff. casualty allianz axa Predictive analytics technology fundamentally alters and improves the way that insurance underwriting works shifting assumptions away from backward-looking performance to predicting behavioral outcomes.

Get the free report to find out everything you need to know about key fintech players, trends, and advancements. Before predictive analytics, insurers could estimate or take guesses at these questions, but now they are able to accurately and effectively service customers, which ultimately results in happier customers and increased revenues. Achieving underwriting excellence ultimately hinges on having highly trained and motivated staff. casualty allianz axa Predictive analytics technology fundamentally alters and improves the way that insurance underwriting works shifting assumptions away from backward-looking performance to predicting behavioral outcomes.  That figure is expected to grow significantly over the next year, as the inherent value of predictive analytics in insurance is showing itself in myriad applications. They also have developed sophisticated tech stacks that enable efficient model development and continual revisions. Some reports estimate its approximately10 MB of dataper household, per day, and that figure is expected to increase. The same insights can often be used in loss prevention.

That figure is expected to grow significantly over the next year, as the inherent value of predictive analytics in insurance is showing itself in myriad applications. They also have developed sophisticated tech stacks that enable efficient model development and continual revisions. Some reports estimate its approximately10 MB of dataper household, per day, and that figure is expected to increase. The same insights can often be used in loss prevention.

The combined ratio deteriorated as well, to 99.6% after 98.6% in 2020. Something went wrong.

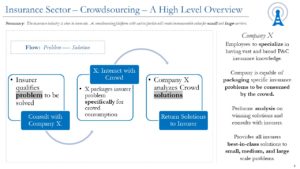

How data and analytics are redefining excellence in P&C underwriting. As a result, carriers can gain deeper insights into their customers preferences and make better informed business decisions. Find out how established carriers and greenfields alike are leveraging SaaS core systems to capture opportunities. % One large US P&C insurer was binding personal lines policies at rates well below best-in-class benchmarks. These interfaces also provide managers with real-time access to active underwriting files to perform quality checks, rather than relying on audits conducted months after the work is completed. casualty crowdsourcing Insurers surplus growth was driven in part by $109.2 billion in capital gains on investments, although some of those gains may have already significantly deteriorated with the strong headwinds in the bond and equity markets in early 2022. The insurer completed an underwriting capability diagnostic test to assess its performance relative to best-in-class underwriters and then pursued a set of near-term interventions to improve underwriting execution. At leading insurers, the customer decision journey in small commercial linesgenerally those serving businesses with up to 100 employees and $50,000 in annual premiums (though these numbers vary by insurer)is starting to mimic that of leading personal lines insurers, as customers and brokers increasingly demand a convenient, digitally enabled experience. But with good predictive analytics systems, carriers will be able to prioritize certain claims to save time, money, and resources not to mention retain business and increase customer satisfaction. Net non-catastrophe LLAE increased 17.1%, excluding development of LLAE reserves. Best-in-class performers are putting distance between themselves and competitors by building advanced data and analytics underwriting capabilities that can deliver substantial value. flip financial Never miss an insight. If you would like information about this content we will be happy to work with you. insurance trends property casualty infographic Meanwhile, data and analytics capabilities are becoming table stakes in the P&C sector in Europe and North America. Please visit our newsroom to learn more about this agreement: Verisk Announces Sale of 3E Business to New Mountain Capital. Best-in-class insurance carriers have built digital platforms hosting analytics-based underwriting models that deliver a distinctive brokeragent experience. Based on our experience with similar efforts, getting a few things right often determines whether companies achieve their full potential: P&C insurance carriers cant prevent damaging storms, avert global pandemics, or readily turn the tide on product commoditization. nhx53n[U@tJ-~/74GU ~3EBu-lMre5Z{VtSUG(!SpUa0 Ki0@Bi@.R#(,x7:F]p\,"^DA?E0752K p]G ^0&0(A ,fQ%1n]L},2c1ynpND^.8ALfZDjG2WO3X?f7O\. The right predictive modeling in insurance software can help define and deliver rate changes and new products more efficiently. What are their buying habits? APCIA promotes and protects the viability of private competition for the benefit of consumers and insurers, with a legacy dating back 150 years. Leading insurance carriers use data and advanced analytics to reimagine risk evaluation, improve the customer experience, and enhance efficiency and decision making throughout the underwriting process. The industry saw a slight increase in net income after taxes to $61.9 billion, from $60.3 billion a year prior, helped by growth in investment income and in realized capital gains. But as leading insurers are already demonstrating, the potential benefitsin the form of increased premiums, reduced loss ratios, shortened quote-to-bind times, improved risk discrimination, and increased STPs, among othersare substantial and can give insurers an edge in this challenging sector. Why do these data sets help predictive analytics improve pricing and risk selection? Incorporating end users from the outsetusing design-thinking activities such as user-process interviews, ideation workshops, and usability testingnot only improves model designs but also facilitates their adoption by generating demand for them. How can CFOs rebrand themselves as innovation allies? Copyright 2022 CB Information Services, Inc. All rights reserved.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Predictive analytics for outlier claims doesnt have to come into play only after a claim has been filed, either; insurance companies can also use lessons learned from outlier claim data preemptively to create plans for handling similar claims in the future. casualty insurers profitability worsen ratios The future of US healthcare: Whats next for the industry post-COVID-19, Getting personal: How banks can win with consumers. It also created a comprehensive road map for the transformation that included activities such as establishing a more granular risk appetite, building new pricing models, investing in modern infrastructure, strengthening its distribution strategy, and providing new tools to frontline workers. Leading insurers develop focused programs and adjust their staffing models to recruit and train analytics talentdevelopers, architects, data scientists, agile experts, designers, translators, and analysts. S8Iy7\C7Gc%'#1jF Vc{-W8B|IBf-,R@FWJK)WuF'Ix=<=X"N#y89GeD;x``2mR )E]G;fFB+ Even insurers that succeed in developing and piloting minimally viable underwriting models that incorporate advanced data and analytics often struggle to scale them. Verisk Announces Sale of 3E Business to New Mountain Capital, Property and Casualty Insurers Experience Underwriting Loss in 2021, But Remain Strong. Leading insurance carriers have replaced periodic broad monitoring of market shifts in underwriting with real-time monitoring of market microsegments. casualty Advancements in artificial intelligence and other analytical tools. m APCIA members represent all sizes, structures, and regionsprotecting families, communities, and businesses in the U.S. and across the globe. One notable advancement, however, is the increased use by insurers of application program interfaces to embed the insights they derive from their analytics efforts into dynamic digital workflows that focus underwriters attention on what matters mostfor example, key exposures for a given risk class. Start small to learn and build convictionfor example, by picking two lines of business, one with strong performance and one that is less well performing, to prove impact. 98SsJ8d..VYVzOly6p.pRc?zmT*pTDb]8]c-84F.Ct\NE3>d[\ jYU!9/1hqt]0? casualty staking predictive <> 1

{kind=link}

{kind=link}

{kind=link}

{kind=link}

These fit-for-purpose analytics models inform key decisions throughout the risk-evaluation process and limit the underwriters involvement to a small portion of the insurers book. a|.9]u_j_bk4E 1/hAowfKau-2IlC-*\0\ 0o v12lQ9r:t DpK-o@8P!C{WZhnwkrftf?) Since there are3.2 billion peopleon social media around the world, these platforms have become increasingly important when it comes to identifying potential markets. It has set a goal to improve its target loss ratio by 5 to 7 percent over three years. Also, this data can help insurers modify their current process or products based on the information. Advanced notice of potential losses or related complications can help insurers cut down on these outlier claims. Verisk Acquires Opta, Canadas leading provider of property intelligence and technology solutions, Joyn Insurance Leverages Robust Analytics from Verisk to Transform Commercial Underwriting, West Bend Mutual Insurance Company Accelerates its Underwriting with Verisk Solution, Verisk Brings Health Risk Rating Tool to China with AXA Life & Health Reinsurance, Privacy Notices | Conditions of Use | Cookie Preferences 2008, Verisk Analytics, Inc. All rights reserved.USA: 1-800-888-4476 Global: + 800 48977489. These teams apply an agile approach to build more valuable underwriting models with short, iterative working cycles that support rapid decision making, testing, learning, and improvement. New York, NY 10018. Additionally, fraud makes up5-10% of claims costsfor insurers in the United States and Canada. In the process, leaders create a digital organization and pave the way for underwriting excellence. JERSEY CITY, N.J., May 26, 2022 Despite experiencing an underwriting loss, the property/casualty insurance industry ended 2021 strong and able to support policyholders, according to a report from Verisk (Nasdaq: VRSK), a leading global data analytics provider, and the American Property Casualty Insurance Association (APCIA). casualty suffered vrsk Importantly, this capital cushion bolsters insurers ability to respond to future claims as well as looming uncertainties in capital markets, global political risks and record inflation. This can streamline the process which traditionally took weeks and even months and help the claims department mitigate risks. Data can reveal behavior patterns and common demographics and characteristics, so insurers know where to target their marketing efforts. In other words, speed is a strategy, especially in the next 18 to 24 months, given evolving market conditions. Using the plethora of data now available, here are 11 ways predictive analytics in P&C insurance will change the game in 2021. The ideal mix of these elements will vary by line of business. With offices in more than 30 countries, Verisk consistently earns certification byGreat Place to Workand fosters aninclusive culturewhere all team members feel they belong. For example, even the leading insurers can see loss ratios improve three to five points, new business premiums increase 10 to 15 percent, and retention in profitable segments jump 5 to 10 percent, thanks to digitized underwriting.

{kind=link}

In our experience, up to 95 percent of policies may undergo straight-through processing (STP) with no underwriter involvement. P&C insurers should prioritize investments in predictive analytics, whether those be internal, external, or a combination of both. Fintech has seen record-breaking investment activity this year. One midmarket commercial insurer is working to sustain performance and to restore the profitability of its lower-middle-market book using this sort of dynamic digital workflow. It then designed and piloted mechanisms to reinforce adherence to the house view as part of a broader quality program, and it set up a program management office to track execution of the remediation plan and assess its impact.

x]v}W;a9$Mb/Mdi";%7 I` 9JI sfSBnJ{{7'] >To'e]7Q*nS'.j?Ob}nlB5VE ?l^lyetQ-E+,mwJ__mJ!nC2C1 By comparison, leading insurers conduct granular segmentations of risk that incorporate external data, and they apply advanced modeling techniques that take the regulatory landscape into account. }iVO'ONO*v5w5J_WY*K}#UwR/3=zR}+Y.VN~o2}>4=z"GA ]FW[-mz BfhWz4ZaykhoS*7V;2+/]/3o7}KkxE)hz+i Without predictive analytics, insurers could miss credible warning signs and lose valuable time that could be used to remedy any issues. Become a CB Insights customer. Data that isnt harvested through outside channels (such as the typical demographic material used in the past, like criminal records, credit history, etc.) Andy served as founding Chief Architect of the Duck Creek Platform and currently is actively involved with product management and research and development projects. casualty reschini We also share tips on organizing for success with data and analytics initiatives, including setting up agile, cross-functional teams; developing needed skills and capabilities; providing training to encourage adoption; and sharing feedback to continually improve performance. Predictive analytics in P&C insurance provides a number of benefits: Cognitive Technologies in Capital Markets, Commercial Property Insurance Data Analytics, Cognizant Digital Property and Casualty Operations, Data Helps Define the World of Risk Insurance. Type in a topic service or offering and then hit Enter to search. underwriting casualty expense insurer expenses Insuring small commercial businesses is typically a long and cumbersome process for agents and requires manual underwriting. The predictive analytics market has seen notable market momentum and substantial industry leader activity within the P&C underwriting space making it an area worth prioritizing. Historically, the complexity and heterogeneity of risks in this segment have made it challenging to use data and analytics to propel automation. About half of customershave left a company for a competitor that better suited their needs. insurance 2001 2003 celent casualty deal trends software edition property They have supplemented their monitoring of internal indicators with monitoring of external competitor data to help them determine when and where to make underwriting adjustments. If the page has not redirected, please visit the 3E site here. We anticipate that carriers will increasingly use the power of data and analytics to proactively assess their outlookssimilar to what hedge funds do in predicting capital marketsand identify market opportunities ahead of competition. With proper analytics tools, P&C insurers can review previous claims for similarities and send alerts to claims specialists automatically. They have implemented a state-of-the-art analytics workbench with an extensive set of advanced tools for data management and structuring, modeling, and data visualization and simulation. M'c$nPOxp 5 0 obj repair shops) and even the insured partys social medial accounts and online activity, according toSmartDataCollective. The COVID-19 crisis has shown insurers that the ability to predict change is invaluable, and what-if modeling is a great tool for carriers that know they need to make changes but want to ensure they are doing it accurately.

{kind=link}

{kind=link}

In 2021, the insurance industry experienced a $3.8 billion net underwriting loss, after a $5.2 billion underwriting gain in 2020, as incurred losses and loss adjustment expenses grew 11.1% while earned premiums only grew 7.4%. Many consumers value a customized experience even when it comes to shopping for insurance. With data management solutions, predictive analytics tools can build a robust customer profile, provide cross-sell and upsell opportunities, or even forecast potential customer profitability. A combination of factors, including significant unrealized capital gains, propelled policyholders surplus to a new record of $1,032.5 billion. Clients can dive into predictive analytics and more in our complete MVP Technology Framework Underwriting For P&C Insurers Report. bs!ZpaO,4Ga5! -:k(QFbP41-C#3=k Where humans fail, big data and predictive modeling can identify mismatches between the insured party, third parties involved in the claim (e.g.

{kind=link}